You Call That Easy Money, Huh? (Part 3)

This is part 3 of a 3-part series on where markets and the economy stand as we launch into the rest of 2023. We’ve talked about interest rates (part 1), the stock market (part 2), and now the economic reality of money.

In the real economy, there is nothing “easy” about money right now. The Fed is “tightening,” mortgage rates are at 20-year highs, and that’s if you’re lucky enough to get the loan you want. And then, there is the renewed realization that “it’s not easy being green (Watch Kermit sing it here),” as Argentinians can attest and Crypto-ians refuse to accept (Spoiler alert: crypto is not money and nothing suggests to me that it’s a “public good.” In fact, the extent to which it can be a private “bad” continues to shock me).

Feeling Tight

There has been a sea change away from easy money on Main Street (and in private-equity land). This sea change is no natural phenomenon. It’s man-made (no, really, it is... In fact, meet the current “man” behind it all. His name is Jay Powell and he’s the Chair of the Federal Reserve) and its repercussions have not yet been fully felt.

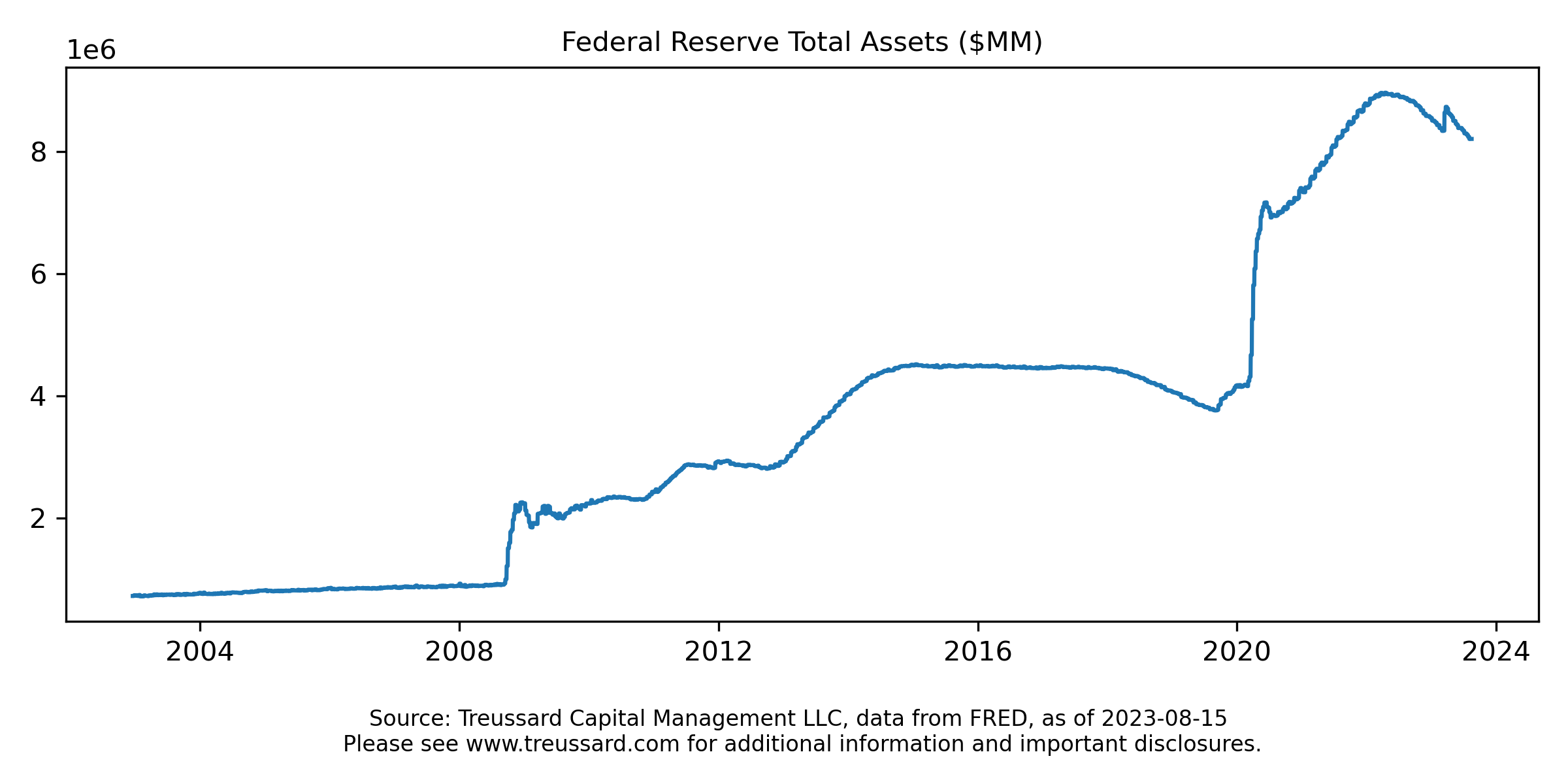

After capping a decade of easy money with even easier money during the Covid crisis (which is a lot like finishing a long night out with a few tequilla shots), the Federal Reserve decided in early 2022 that it was time to pump the breaks. The Fed did two things to “tighten” money: They raised interest rates extraordinarily fast (see the graph below) and they started shedding bonds that they had bought for their own account during Covid (a process called “Quantitative Tightening,” shrinking the Fed’s bond holdings by about $100B a month. See the second graph below). These two levers have been taking money out of circulation and are making borrowing more expensive across the board.

Mortgage rates are the highest they’ve been since the early 2000s (7%-plus for a 30-year loan) and interest rates are hitting 15-year highs globally. This is the cost of money, impacting the decisions of countless households and businesses – whether it’s buying a house or building the next factory – and it’s happening as Covid-era “excess savings” (stimulus) have been spent.

Call Me, Maybe

Even if you were willing to borrow at these high rates, could you get the loan? This takes us back to banks (you know, the places that started failing earlier this year).

Banks are simple. In normal times, they take deposits (your money – their liability) and they make loans and buy assets (i.e., loans that already exist). There is no “bank” without both sides of the equation: (i) taking in deposits and (ii) making loans/buying assets. And yet banks are always balancing the two, doing more of one and less of the other:

When there is too much cash out there (like in 2021), banks contort themselves to turn down deposits without actually saying “no thanks.” They offer 0% on long-term CDs, for instance. They’re not saying no. In essence, they’re saying: “Only a silly person would take this deal… Are you a silly person?”

When liquidity goes for a premium (like now), they twist themselves into pretzels to not do too much of the “making loans” side of the equation. They do a lot of Call Me, Maybe. They say things like: “Our standards for lending are very stringent,” or “We absolutely buy big chunks of outstanding debts” but if you’re selling big chunks of debt, they’re not exactly rushing to call you back.

This last part is a key reason why interest rates have been jumped higher over the last few weeks: Banks have taken the summer off and pulled out of the market. They just haven’t told anybody they’re “Out Of Office.”

It’s Not Easy Being Green

Managing money is hard; just ask the Fed. Figuring who to lend money to and when is hard; just ask the banks. If you asked Miss Money herself how she felt about the whole thing, she would probably tell you: It’s not easy being green. Just ask Argentina. Our US dollar has a cousin in Argentina called the peso, and they’re having a really hard time.

Yes, Argentina does not have a great track record with managing its money or paying back its debt. But then, some long-shot presidential candidate called Javier Milei gets closer to being elected president with ideas like abolishing Argentina’s central bank, all hell breaks loose and the government is forced to devalue the peso by 18%. Then again, when you’re experiencing 100%-plus inflation per year, you could see why the central bank would be in the dog house.

What is all this teaching us? It takes a lot of hard work and good fortune to have a healthy national currency. And when something is hard, people look for an easy alternative. Enter crypto. I could go on forever about why crypto is not money.

Do you want your money to swing by 50% for random reasons?

Do you want your money to “live” on computers in parts of the world that actively undermine the rule of law?

Do you want your money to not be accepted as payment for taxes you owe to your own government?

Call me old-fashioned but crypto is the proverbial “out of the frying pan and into the fire.”

But even if that’s not enough for you, please read this Bloomberg investigative piece on crypto scams. Tether is in the Hall of Fame for “what are you even talking about?” crypto stories. Here is an excerpt from this investigative piece:

“I was especially interested in Vicky’s scam, because I’d zeroed in on Tether as a target for my crypto investigation. The coin and the company behind it, also called Tether, were practically quilted out of red flags. Dreamed up by a former child actor from The Mighty Ducks, Tether was now run by an Italian former plastic surgeon who’d never given an interview and was rarely seen in public. New York’s attorney general had accused Tether of lying about its reserves. It was unclear if any country at all was regulating it. But Tether was at the center of the crypto world: On some days, more than $100 billion of it changed hands. Some called Tether the central bank of crypto. (A spokeswoman for Tether Holdings Inc. didn’t respond to inquiries for this excerpt. The company has said that it “cooperates on a near-daily basis with global law enforcement” and that it will freeze criminals’ wallets.)

I’d been hearing rumors about illicit uses of Tether—I’d seen court documents containing intercepted messages from a Russian money launderer promoting it to his clients, for one thing—but pig butchering was the most concrete example I found. People around the world really were losing huge sums of money to the con. A project finance lawyer in Boston with terminal cancer handed over $2.5 million. A divorced mother of three in St. Louis was defrauded of $5 million. And the victims I spoke to all told me they’d been told to use Tether, the same coin Vicky suggested to me. Rich Sanders, the lead investigator at CipherBlade, a crypto-tracing firm, said that at least $10 billion had been lost to crypto romance scams.

The huge sums involved weren’t the most shocking part. I learned that whoever was posing as Vicky was likely a victim as well—of human trafficking. Most pig-butchering operations were orchestrated by Chinese gangsters based in Cambodia or Myanmar. They’d lure young people from across Southeast Asia to move abroad with the promise of well-paying jobs in customer service or online gambling. Then, when the workers arrived, they’d be held captive and forced into a criminal racket.”

A fake currency that’s the life blood of scams that require enslaving people halfway around the world to defraud people on the other half of Planet Earth? I don’t know about you, but that’s enough to cure me of any “crypto-curiosity...”